Suppose you’ve decided that this is the year you’re finally going to spring for new skis. Let’s add to this scenario the likelihood that you’d prefer to get a good deal on your prospective purchase. To help guide you through the thicket of decisions in front of you, let’s first get a big-picture look at what the U.S. market for men’s alpine skis looks like for the 2026 season.

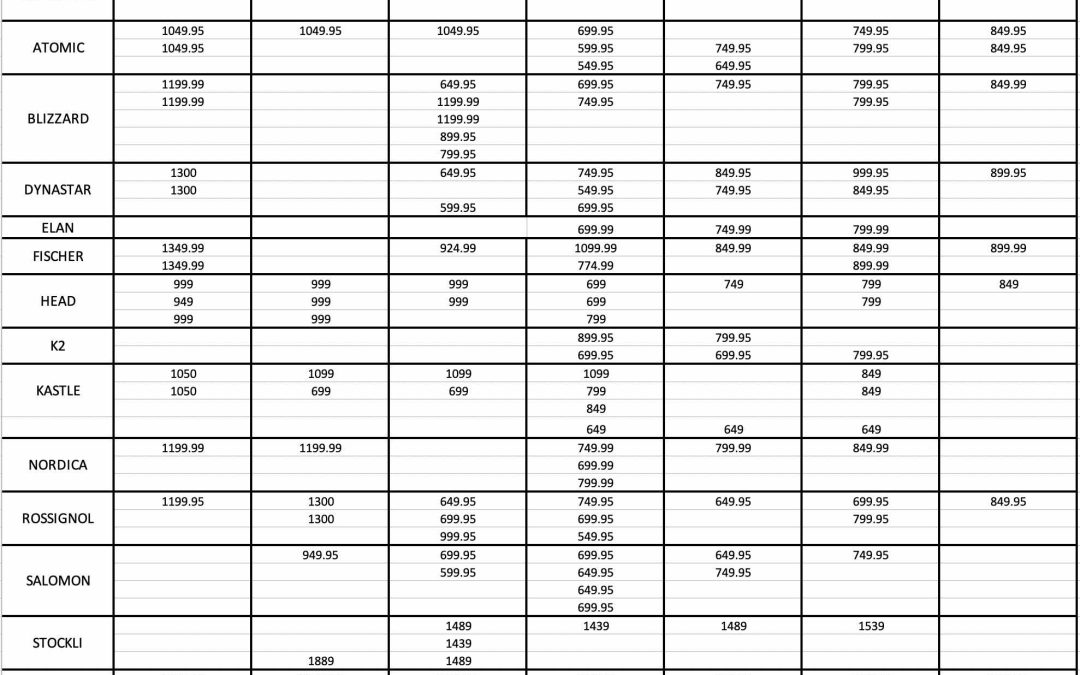

To get an overview of today’s ski-pricing panorama, I’ve sorted the current market by brand and genre, using category definitions that key off the waist width boundaries I established over a decade ago. I’ve replaced the model names with their respective Minimum Advertised Price (MAP) for easy comparison across brands. Let’s take a deep dive into the price structure of the market as a whole, beginning with the Non-FIS Race column.

Once upon a time, racing and recreational skiing were closely linked in terms of both product and culture, but that world has long since ceased to exist. Now alpine racing is a world unto itself, with little correlation to most of the rest of the ski world, and this unbridgeable divide carries over to the price grid. Most brands sell the race skis they allow the general public to buy at suggested retail, period. Any special pricing is restricted to programs that control what is sold to whom and at what price. In any case, no one in their right mind buys a race ski, FIS-sanctioned or not, based on price. As I said, it’s a totally different world.

The Technical genre is alive and well in Europe but dead as a doornail in the U.S. As with the NFR genre, prices are unflinchingly high. The only below-the-norm price that jumps off the page comes from Kästle, who concocted its new M9 series specifically as a low-cost alternative to its far pricier kin, the fabled MX series. At the other end of the pricing spectrum, Stöckli’s Laser SX is unabashedly well above the norm.

The Frontside market is by far the most diverse in every respect, serving every skier from never-evers to the technically flawless. Most Frontside models are system skis, meaning they come with their own binding, which usually is reflected in a $200 price bump over the same ski flat (i.e., no binding). There’s a fully populated netherworld of Frontside system skis made to hit commercially popular price points that aren’t on this grid, as all brands that engage in this segment follow similar pricing/performance guidelines.

As we move to the right side of the pricing matrix, we’re into product families with siblings in every price slot. In the All-Mountain genres, where most skis are sold in this country, two factors dominate the price segmentation picture: width – as a rule, wider skiers cost more – and the introduction of alternative model families to increase brand penetration of the most important – and profitable – categories. The customary rationale for two model families spread over four categories is that one will be biased towards mixed, off-trail conditions while the other will retain elite carving/groomed terrain attributes.

So, what does this price grid tell us about the market where you’re currently searching for your next ski? First of all, there’s no point in shopping for a new ski based on price. The prices for comparable skis are all virtually the same, close enough to qualify for price fixing, not that anyone in the current regulatory climate gives a hoot. Sure, there’s a $50 difference here and there, BUT DO NOT BASE ANY SKI (OR BOOT OR BINDING) BUYING DECISION ON A $50 DIFFERENCE. Considering how long you’re going to own your new skis, a $50 price difference doesn’t mean diddley.

If you were to compare this grid to a parallel exercise on last season’s MAP pricing, you’d find that even crippling tariffs didn’t move ski prices significantly upward. The facts are, both retailers and suppliers are trying hard to keep prices tethered to the same price points that have prevailed for over a decade. The principal force keeping a cap on retail pricing is fear of a consumer backlash that will signal a massive market retreat. While such concerns aren’t unfounded, the most price-sensitive participants have already been flushed out of what was once a middle-class sport. But most suppliers continue to act as though the skier population is shrinking, at a time when participation seems to be holding at or near all-time highs.

Allow me to hasten to point out that just because 10 companies all sell a ski intended to retail at, say, $799, that all such skis will perform equally well. There’s nothing preventing a brand from making a sub-standard product and slipping it into an inventory comprised mostly of better-made models. As costs increase, so will the temptation to skimp on construction in order to keep retail pricing in check. We may have reached the point where suppliers will face tough choices about whether to increase price, degrade quality or just drop a product from its catalog.

If not now, when?

With the notable exception of Stöckli, most skis in a given genre are priced within $50 of their competitors, at least on paper. This will be the status quo through the fall for all new skis, but the same rules don’t apply to carryover inventory. The fall season is one of the best times to shop for a discontinued or used ski because the seller is motivated to liquidate second-hand stock. The largest and most successful ski swaps in America do most of their business in October, so if you know what you’re looking for, it’s a great time to pounce on a deal.

There’s only one drawback to buying pre-season: you won’t be able to demo the ski before adopting it. This needn’t be a deal-breaker, but if you really want a new ski at the best price, you might as well wait until after the holidays. The best deal on a new ski won’t materialize until late February, when vendor rules on pricing policies lower the MAP price, which means you’ll have all of January and most of February to try every model on your hit list. This wait-to-buy mentality is right in line with current consumer tendencies to defer major purchases until the last minute. The longer one waits, the more the average sale price will decline until the season is over.

While the demo-before-you-buy program is recommended, there’s always the risk, however slight, that the model you finally fall for will be sold out. Given the perennially over-stocked position of the last few seasons, it might be hard to imagine a model selling to the wall, but the surpluses of the past are finally receding, and early indications are that retailers will be buying conservatively given an uncertain economic environment.

So, what did we learn from this exercise? Take-away number one has to be the market trend towards price parity within any given non-race category. Conclusion number two: the best time to buy a new ski is either early, when selection is at its peak, or late, when price competition among retail outlets intensifies. Your best shot at used gear or discontinued models occurs during the fall swap period, typically sometime in October. This may sound like a crazy way to operate, but it wouldn’t have evolved in this direction if the major brands didn’t want it that way. The U.S. ski market has been following this pattern of pricing parity and sell-through guidelines for over a decade. It’s unlikely to change in the foreseeable future.

Related Articles

It’s About Nothing

In the last week of January,2009 I was able to spend a few days skiing in Little Cottonwood Canyon, which is always cathartic for my ravaged soul. The conditions were all over the map, the mountains having experienced a long, hot spell followed by rain, grapple, wet snow and finally dry snow driven by winds that could flense an adult walrus in a few minutes. Couldn’t have been better.

I had been preparing for the trip for weeks, psychologically. Two back surgeries the previous winter had reduced my training regimen from semi-annual to non-existent. Scheduling conflicts such as work kept me from visiting the areas that abound at home near Lake Tahoe, so I had zero ski days on a body with more fat on it than a French duck. I had as much chance of surviving Snowbird and Alta as a rib roast in a piranha tank.

Fortunately, the Lord is merciful, anti-inflammatory drugs are powerful and there are techniques that allow one to block out pain. There are also many wonderful people in this world with which to ski, kind people who stand quietly by, pretending to be in awe of Nature, while my chest heaves so violently in its futile quest for oxygen that tiny lung particles break lose and make for the exits. One such person is Guru Dave Powers, a man whose passion for the sport hasn’t diminished after thousands of days of riding gravity down the infinitely variable slopes and crannies of Snowbird. The Goo knows this hill, and in knowing it well knows so much more.

The Making of a Skier, Chapter XII: Putting Words into the Mouth of God & Other Mid-Life Adventures

When I was cut adrift by Head on June 13, 2001, my once glowing prospects dimmed considerably. The date is etched in memory because I hosted a small soirée that evening in honor of my darling wife’s 50th birthday. One of the attendees was Paul Hochman, who would play several roles in my life as I wandered in the wilderness of unemployment during what were supposed to be my peak earning years.

During the gaping hole in my career that spanned 2001-2011, I would eventually spend every cent of my inheritance, plus most of what I’d saved from earlier bouts with gainful employment, just keeping the household afloat. Despite a river of red ink, my resume would suggest that I was not only commercially active during this epoch, but had my hand in all sorts of ventures.

Fit the Whole Skier

We bootfitters are naturally obsessed with feet, but the best bootfitters don’t just fit feet; they fit the whole skier. The “whole skier” includes more than just a quick survey of the lower leg and how it’s connected to the foot. It’s even more than all of the skier’s physical attributes, which include not only height and weight, but seated posture, stance, kinesthetic wiring, arch health and stiffness throughout the kinetic chain; the whole skier also includes his or her history with the sport and, most importantly, what sort of skier he or she wants to be.

One of the most obvious traits about almost all boot customers is his or her gender. (Please forgive me if I don’t overcomplicate what should be a simple point about body type.) The first step in a sales process that consists of winnowing all possible boots down to one is picking from the pile of unisex boots or the alternative world of women’s boots.

No-brainer, right? Not so fast. What if a particular woman were tall, with a long tibia and a tapered calf? Let’s add to her profile that she’s a good athlete with a background in dance. Up to now, she’s only been an occasional skier who rented her gear, but a new beau has persuaded her to take a deeper dive. She already has her season pass.