Suppose you’ve decided that this is the year you’re finally going to spring for new skis. Let’s add to this scenario the likelihood that you’d prefer to get a good deal on your prospective purchase. To help guide you through the thicket of decisions in front of you, let’s first get a big-picture look at what the U.S. market for men’s alpine skis looks like for the 2026 season.

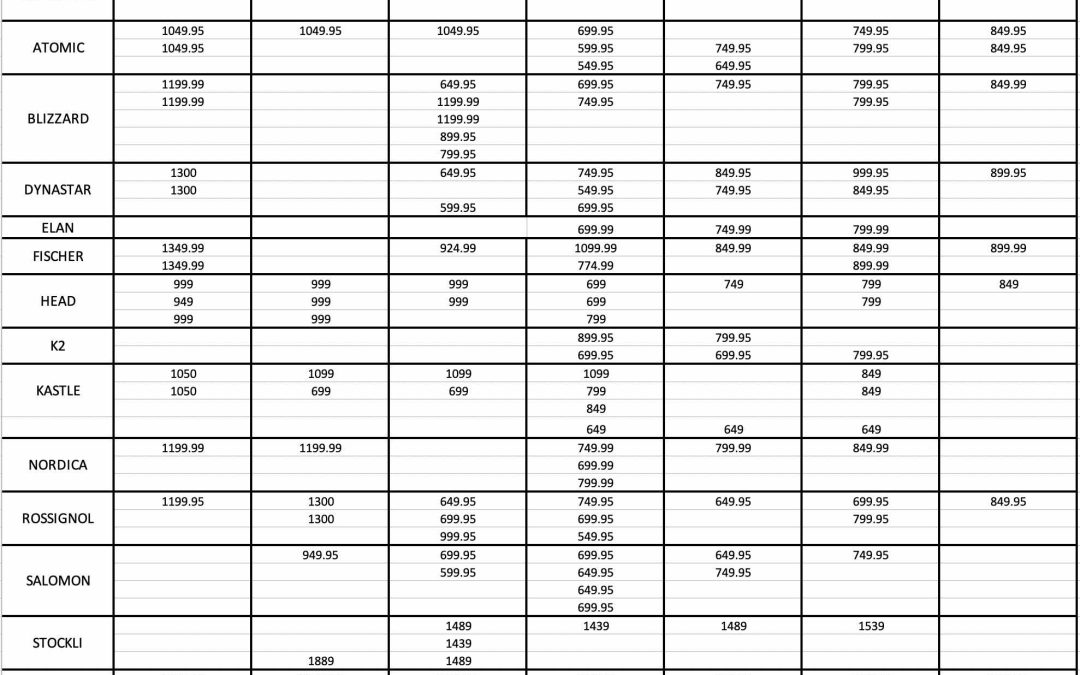

To get an overview of today’s ski-pricing panorama, I’ve sorted the current market by brand and genre, using category definitions that key off the waist width boundaries I established over a decade ago. I’ve replaced the model names with their respective Minimum Advertised Price (MAP) for easy comparison across brands. Let’s take a deep dive into the price structure of the market as a whole, beginning with the Non-FIS Race column.

Once upon a time, racing and recreational skiing were closely linked in terms of both product and culture, but that world has long since ceased to exist. Now alpine racing is a world unto itself, with little correlation to most of the rest of the ski world, and this unbridgeable divide carries over to the price grid. Most brands sell the race skis they allow the general public to buy at suggested retail, period. Any special pricing is restricted to programs that control what is sold to whom and at what price. In any case, no one in their right mind buys a race ski, FIS-sanctioned or not, based on price. As I said, it’s a totally different world.

The Technical genre is alive and well in Europe but dead as a doornail in the U.S. As with the NFR genre, prices are unflinchingly high. The only below-the-norm price that jumps off the page comes from Kästle, who concocted its new M9 series specifically as a low-cost alternative to its far pricier kin, the fabled MX series. At the other end of the pricing spectrum, Stöckli’s Laser SX is unabashedly well above the norm.

The Frontside market is by far the most diverse in every respect, serving every skier from never-evers to the technically flawless. Most Frontside models are system skis, meaning they come with their own binding, which usually is reflected in a $200 price bump over the same ski flat (i.e., no binding). There’s a fully populated netherworld of Frontside system skis made to hit commercially popular price points that aren’t on this grid, as all brands that engage in this segment follow similar pricing/performance guidelines.

As we move to the right side of the pricing matrix, we’re into product families with siblings in every price slot. In the All-Mountain genres, where most skis are sold in this country, two factors dominate the price segmentation picture: width – as a rule, wider skiers cost more – and the introduction of alternative model families to increase brand penetration of the most important – and profitable – categories. The customary rationale for two model families spread over four categories is that one will be biased towards mixed, off-trail conditions while the other will retain elite carving/groomed terrain attributes.

So, what does this price grid tell us about the market where you’re currently searching for your next ski? First of all, there’s no point in shopping for a new ski based on price. The prices for comparable skis are all virtually the same, close enough to qualify for price fixing, not that anyone in the current regulatory climate gives a hoot. Sure, there’s a $50 difference here and there, BUT DO NOT BASE ANY SKI (OR BOOT OR BINDING) BUYING DECISION ON A $50 DIFFERENCE. Considering how long you’re going to own your new skis, a $50 price difference doesn’t mean diddley.

If you were to compare this grid to a parallel exercise on last season’s MAP pricing, you’d find that even crippling tariffs didn’t move ski prices significantly upward. The facts are, both retailers and suppliers are trying hard to keep prices tethered to the same price points that have prevailed for over a decade. The principal force keeping a cap on retail pricing is fear of a consumer backlash that will signal a massive market retreat. While such concerns aren’t unfounded, the most price-sensitive participants have already been flushed out of what was once a middle-class sport. But most suppliers continue to act as though the skier population is shrinking, at a time when participation seems to be holding at or near all-time highs.

Allow me to hasten to point out that just because 10 companies all sell a ski intended to retail at, say, $799, that all such skis will perform equally well. There’s nothing preventing a brand from making a sub-standard product and slipping it into an inventory comprised mostly of better-made models. As costs increase, so will the temptation to skimp on construction in order to keep retail pricing in check. We may have reached the point where suppliers will face tough choices about whether to increase price, degrade quality or just drop a product from its catalog.

If not now, when?

With the notable exception of Stöckli, most skis in a given genre are priced within $50 of their competitors, at least on paper. This will be the status quo through the fall for all new skis, but the same rules don’t apply to carryover inventory. The fall season is one of the best times to shop for a discontinued or used ski because the seller is motivated to liquidate second-hand stock. The largest and most successful ski swaps in America do most of their business in October, so if you know what you’re looking for, it’s a great time to pounce on a deal.

There’s only one drawback to buying pre-season: you won’t be able to demo the ski before adopting it. This needn’t be a deal-breaker, but if you really want a new ski at the best price, you might as well wait until after the holidays. The best deal on a new ski won’t materialize until late February, when vendor rules on pricing policies lower the MAP price, which means you’ll have all of January and most of February to try every model on your hit list. This wait-to-buy mentality is right in line with current consumer tendencies to defer major purchases until the last minute. The longer one waits, the more the average sale price will decline until the season is over.

While the demo-before-you-buy program is recommended, there’s always the risk, however slight, that the model you finally fall for will be sold out. Given the perennially over-stocked position of the last few seasons, it might be hard to imagine a model selling to the wall, but the surpluses of the past are finally receding, and early indications are that retailers will be buying conservatively given an uncertain economic environment.

So, what did we learn from this exercise? Take-away number one has to be the market trend towards price parity within any given non-race category. Conclusion number two: the best time to buy a new ski is either early, when selection is at its peak, or late, when price competition among retail outlets intensifies. Your best shot at used gear or discontinued models occurs during the fall swap period, typically sometime in October. This may sound like a crazy way to operate, but it wouldn’t have evolved in this direction if the major brands didn’t want it that way. The U.S. ski market has been following this pattern of pricing parity and sell-through guidelines for over a decade. It’s unlikely to change in the foreseeable future.

Related Articles

Is 3D Imaging a Fad or the Future?

Any serious attempt at bootfitting begins with an assessment of the customer’s feet and lower legs. This appraisal can be as superficial as measuring each foot for length or as detailed as a complete skier profile accompanied by a few basic biomechanical evaluations.

Better bootfitters gather further information from a litany of details that lie outside the scope of the usual foot-measuring device, such as a Brannock. The veteran bootfitter watches how the customer walks, sits and assumes a skiing position, for starters. The savvy fitter can even spot limb-length differences and redistribute pressure around the foot in places no measuring stick can quantify.

If this sounds like a pretty sophisticated skill set, well, it is. Yet many, if not most, prospective boot buyers approach the bootfitting exercise with the same enthusiasm they usually reserve for a root canal. Suspicions are often confirmed when the first boot proffered seems crazily short. Even the most knowledgeable fitter is obliged to re-establish his/her credibility just to move the bootfit process pass square one.

Of Podcasts, Archives & Revelations

According to my tight-knit circle of advisors, idolaters, sycophants and astrologers, I was made for this medium.

Of course, any garden-variety sycophant will whisper words of inspirational twaddle, but the faint note of sincerity I detect in the smarm-storm of platitudes meant to buck me up has proven sufficient to spur me to action. I quickly acquired a very professional looking microphone and a pop filter to knock down my fierce sibilants. To preserve my objectivity, I opted not to take any lessons, follow any tutorials or otherwise prepare myself for this venture. By the powers vested in me as the Pontiff of Powder, I declare myself to be, now and forever after, a podcaster.

I’ll give you a moment to recover.

The Making of a Skier, Chapter XI: Desperate Measures

When Head humanely, if rather brusquely, terminated my tenure in 2001, the ski business in the U.S. was already facing stiff headwinds, a brewing storm that would turn into a full-on debacle when 9/11 disrupted all commerce. I became unemployed just in time for the job market to implode.

I don’t handle inactivity well. I started writing a very long, very dreadful novel, composed a handful of scripts for Warren Miller – and later, Jeremy Bloom – to recite and scribbled batches of brochure copy and white papers for industries as diverse as accounting software, instrumented football helmets that registered concussions and risk assessment based on location.

The pickings were slim, but they wouldn’t have amounted to anything at all were it not for a little help from my friends. Andy Bigford, who I’d worked with at Snow Country, hired me for the Warren Miller gig. A college chum kindly engaged me to write white papers on accounting fraud. But it was Dave Bertoni, an erstwhile colleague from Salomon days, who joined me in creating Desperate Measures: A Training Method for Selling Technical Products at Retail.